Factor 2020 Cost-of-Living Adjustments into Your Year-End Tax Planning

The IRS recently issued its 2020 cost-of-living adjustments. With inflation remaining largely in check, many amounts increased slightly, and some stayed at 2019 levels. As you implement 2019 year-end tax planning strategies, be sure to take these 2020 adjustments into account in your planning.

Also, keep in mind that, under the Tax Cuts and Jobs Act (TCJA), annual inflation adjustments are calculated using the chained consumer price index (also known as C-CPI-U). This increases tax bracket thresholds, the standard deduction, certain exemptions and other figures at a slower rate than was the case with the consumer price index previously used, potentially pushing taxpayers into higher tax brackets and making various breaks worth less over time. The TCJA adopts the C-CPI-U on a permanent basis.

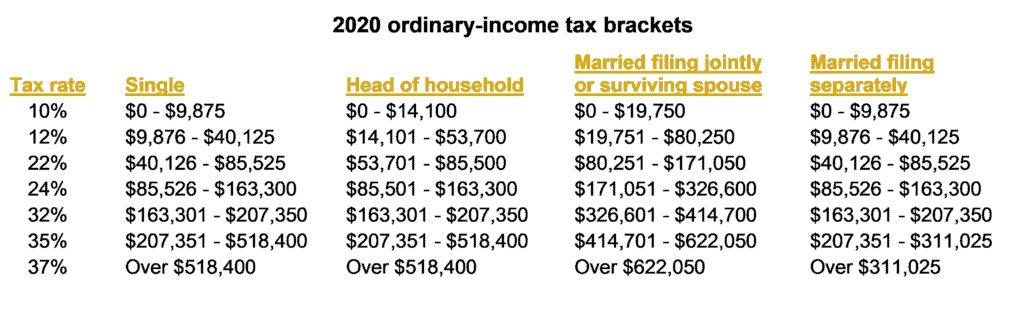

Individual income taxes

Tax-bracket thresholds increase for each filing status but, because they’re based on percentages, they increase more significantly for the higher brackets. For example, the top of the 10% bracket increases by $175 to $350, depending on filing status, but the top of the 35% bracket increases by $8,100 to $9,700, again depending on filing status.

The Tax Cuts and Jobs Act (TCJA) suspended personal exemptions through 2025. However, it nearly doubled the standard deduction, indexed annually for inflation through 2025. For 2020, the standard deduction is $24,800 (married couples filing jointly), $18,650 (heads of households), and $12,400 (singles and married couples filing separately). After 2025, standard deduction amounts are scheduled to drop back to the amounts under pre-TCJA law.

Changes to the standard deduction could help some taxpayers make up for the loss of personal exemptions. But it might not help a lot of taxpayers who typically itemize deductions.

AMT

The alternative minimum tax (AMT) is a separate tax system that limits some deductions, doesn’t permit others and treats certain income items differently. If your AMT liability is greater than your regular tax liability, you must pay the AMT.

Like the regular tax brackets, the AMT brackets are annually indexed for inflation. For 2020, the threshold for the 28% bracket increased by $3,100 for all filing statuses except married filing separately, which increased by half that amount.

The AMT exemptions and exemption phaseouts are also indexed. The exemption amounts for 2020 are $72,900 for singles and heads of households and $113,400 for joint filers, increasing by $1,200 and $1,700, respectively, over 2019 amounts. The inflation-adjusted phaseout ranges for 2020 are $518,400–$810,000 (singles and heads of households) and $1,036,800–$1,490,400 (joint filers). Amounts for separate filers are half of those for joint filers.

Education and child-related breaks

The maximum benefits of various education- and child-related breaks generally remain the same for 2020. But most of these breaks are limited based on a taxpayer’s modified adjusted gross income (MAGI). Taxpayers whose MAGIs are within the applicable phaseout range are eligible for a partial break — and breaks are eliminated for those whose MAGIs exceed the top of the range.

The MAGI phaseout ranges generally remain the same or increase modestly for 2020, depending on the break. For example:

- The American Opportunity credit. The MAGI phaseout ranges for this education credit (maximum $2,500 per eligible student) remain the same for 2020: $160,000–$180,000 for joint filers and $80,000–$90,000 for other filers.

- The Lifetime Learning credit. The MAGI phaseout ranges for this education credit (maximum $2,000 per tax return) increase for 2020. They’re $118,000–$138,000 for joint filers and $59,000–$69,000 for other filers — up $2,000 for joint filers and $1,000 for others.

- The adoption credit. The MAGI phaseout ranges for eligible taxpayers adopting a child will also increase for 2020 — by $3,360 to $214,520–$254,520 for joint, head-of-household and single filers. The maximum credit increases by $220, to $14,300 for 2020.

(Note: Married couples filing separately generally aren’t eligible for these credits.)

These are only some of the education- and child-related breaks that may benefit you. Keep in mind that, if your MAGI is too high for you to qualify for a break for your child’s education, your child might be eligible to claim one on his or her tax return.

Gift and estate taxes

The unified gift and estate tax exemption and the generation-skipping transfer (GST) tax exemption are both adjusted annually for inflation. For 2020, the amount is $11.58 million (up from $11.40 million for 2019).

The annual gift tax exclusion remains at $15,000 for 2020. It’s adjusted only in $1,000 increments, so it typically increases only every few years. (It increased to $15,000 in 2018.)

Retirement plans

Not all of the retirement-plan-related limits increase for 2020. Thus, you may have limited opportunities to increase your retirement savings if you’ve already been contributing the maximum amount allowed:

Your MAGI may reduce or even eliminate your ability to take advantage of IRAs. Fortunately, IRA-related MAGI phaseout range limits all will increase for 2020:

Traditional IRAs. MAGI phaseout ranges apply to the deductibility of contributions if a taxpayer (or his or her spouse) participates in an employer-sponsored retirement plan:

For married taxpayers filing jointly, the phaseout range is specific to each spouse based on whether he or she is a participant in an employer-sponsored plan:

- For a spouse who participates, the 2020 phaseout range limits increase by $1,000, to $104,000–$124,000.

- For a spouse who doesn’t participate, the 2020 phaseout range limits increase by $3,000, to $196,000–$206,000.

- For single and head-of-household taxpayers participating in an employer-sponsored plan, the 2020 phaseout range limits increase by $1,000, to $65,000–$75,000.

Taxpayers with MAGIs within the applicable range can deduct a partial contribution; those with MAGIs exceeding the applicable range can’t deduct any IRA contribution.

But a taxpayer whose deduction is reduced or eliminated can make nondeductible traditional IRA contributions. The $6,000 contribution limit (plus $1,000 catch-up if applicable and reduced by any Roth IRA contributions) still applies. Nondeductible traditional IRA contributions may be beneficial if your MAGI is also too high for you to contribute (or fully contribute) to a Roth IRA.

Roth IRAs. Whether you participate in an employer-sponsored plan doesn’t affect your ability to contribute to a Roth IRA, but MAGI limits may reduce or eliminate your ability to contribute:

For married taxpayers filing jointly, the 2019 phaseout range limits increase by $3,000, to $196,000–$206,000.

For single and head-of-household taxpayers, the 2019 phaseout range limits increase by $2,000, to $124,000–$139,000.

You can make a partial contribution if your MAGI falls within the applicable range, but no contribution if it exceeds the top of the range.

(Note: Married taxpayers filing separately are subject to much lower phaseout ranges for both traditional and Roth IRAs.)

Crunching the numbers

With the 2020 cost-of-living adjustment amounts inching slightly higher than 2019 amounts, it’s important to understand how they might affect your tax and financial situation. We’d be happy to help crunch the numbers and explain the best tax-saving strategies to implement based on the 2020 numbers.

© 2019